conomic Update:

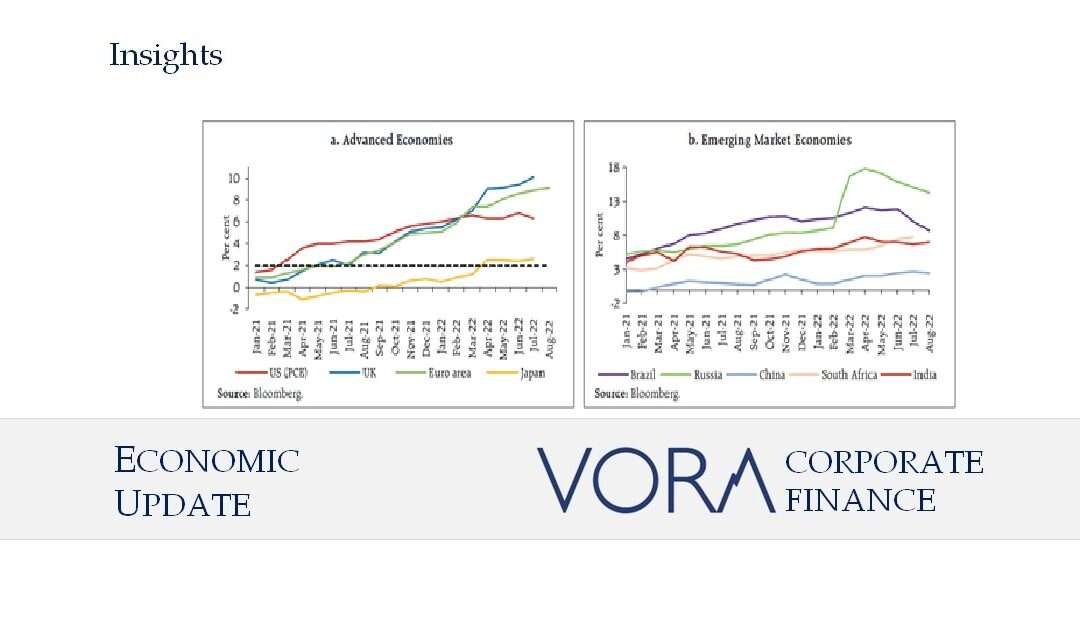

- The RBI’s monetary policy committee raised the policy repo rate on September 30, 2022 by 50 bps a total of 190 basis point, its fourth hike in the current cycle, as India’s annual inflation rate came above the central bank’s target band for the eighth consecutive month in August, driven by surging food prices.

- Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.65 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 6.15 per cent.

- MPC said that it is focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

- MPC believes that the inflation is likely to be above the upper tolerance level of 6% till Q3 2023 due to considerable uncertainty, given the volatile geopolitical situation, global financial market volatility and supply disruptions.

- CPI inflation rose to 7.0 per cent (y-o-y) in August 2022 from 6.7 per cent in July as food inflation moved higher. 7.6% in rural India and 7.55% in urban parts of the country, from around 6.7% in July.

Policy change by US Fed:

- US Federal Reserve raised interest rates by 75 basis points for the second straight month.

- As the COVID-19 pandemic emerged in March 2020, the Fed implemented an aggressive quantitative easing strategy, injecting more than $700 billion in asset purchases, and by June 2020 established a QE program to purchase $80 billion in Treasury securities and $40 billion in mortgage-backed securities per month.

- The Fed started tapering its large-scale asset purchases in December 2021, the economy showed significant strength and a cost-of-living surge.

- The Fed started quantitative tightening in June, capping the decline at $30 billion in Treasuries and $17.5 billion per month in agency mortgage-backed securities (MBS).

- In June 2022, the Federal Reserve changed its monetary policy direction to manage the threat of rising costs. The Fed revised its position after two years of an “easy money” policy, ending its policy of low-interest rates and significant intervention in the bond market.

Rupee Depreciation against USD:

- As US Fed increases rates, Global investors would prefer US markets to invest as it is offering higher interest rates. As global funds flow to US, this would reduce the demand for other emerging or European market currencies and make their currencies depreciate.

- Sharp increase by US Feds have thus resulted depreciation of all major currencies across world. Rupee too has depreciated by 7.4% to Rs 81 against 1 USD. About 67 per cent of the decline in reserves during the current financial year is due to valuation changes arising from an appreciating US dollar and higher US bond yields.

- A depreciating rupee will pressurize the inflation rates more as the costs of key imported goods like food and crude and services will be higher. And, as the dollar gains strength, there will be increased outflows in the foreign investments. This will also lead to widening India’s trade deficit. Whereas, it will be favorable for exports. This will also lead to widening India’s trade deficit.

- RBI has actively sold dollars to counter rupee depreciation. RBI maintains that it is selling dollars to reduce volatility in FOREX markets, but India’s FOREX reserves have come down to $550 Bn from a high of $642 Bn.

- RBI’s recent hike in repo rate is also partly to address the rupee depreciation. However primary reason to increase repo rate is to tackle inflation which is higher than upper tolerance level of 6%.

Acknowledgements:

RBI Bulletin (www.bulletin.rbi.org.in), SEBI (www.sebi.gov.in), NSE (www.nseindia.com), BSE (www.bseindia.com)

Disclaimer:

This material has been prepared by the personnel in Vora Corporate Finance which is Investment Banking arm of Vora Management Consultancy Private Limited and looks after Mergers & Acquisitions (M&A), Private Equity (PE), Fund Raising, Debt syndication and Valuations and is based out of Ahmedabad, Gujarat, India. Any views or opinions expressed herein are solely that of individual authors and may differ from view of Vora Management Consultancy Private Limited. This material is proprietary to Vora Management Consultancy Private Limited and is for your personal use only. Any distribution, copy, reprints or forward to others is strictly prohibited.

This material captures the information based on information available in the public domain, public announcements and sources believed to be reliable. Analysis contained herein is based on publicly available information and appropriate assumptions. This material is intended merely to highlight market developments and is not intended to be comprehensive and does not constitute strategic, investment, legal or tax advice. In no event Vora Management Consultancy Private Limited be liable for any use by any party or for any decision made or action taken by any party in reliance upon, or for any inaccuracies or errors in, or omissions from, the information contained herein and such information may not be relied upon by you for evaluating any transaction.

#mergersandacquisitions #privateequity #ipo #debt #debtsyndication #valuations #rating #creditrating #financeadvisory #finance #economy #indianeconomy #fundraising #capitalmarket #capital #banking #m&a #ma #pe #initialpublicoffer #businessloan #loan #businessvaluation #registeredvaluer #acquisition #merger #deals #financialdeals #ahmedabad #gujarat #india #ratingadvisory#primarymarket #secondarymarket #mergersandacquisitionsahmedabad #maahmedabad #privateequityahmedabad #ipoahmedabad #financeadvisoryahmedabad #stockmarket